Under current law, CBO projects, Social Security’s trust funds, considered together, will be exhausted in 2029. In that case, benefits in 2030 would need to be reduced by 29 percent from the scheduled amounts.

Source: CBO *** What Is the Outlook for Social Security Spending and Revenues?

In 2010, for the first time since the enactment of the Social Security Amendments of 1983, annual outlays for the program exceeded annual revenues (excluding interest) credited to the combined OASDI trust funds. A gap between those amounts has persisted since then, and in fiscal year 2016, total outlays exceeded noninterest income by about 7 percent. As more people in the baby-boom generation retire over the next few decades and as longer life spans lead to longer retirements, that gap will widen, CBO projects. If current laws governing taxes and spending stayed the same and if benefits were paid as scheduled, outlays for the Social Security program would rise from 5.0 percent of gross domestic product (GDP) in 2016 to 5.9 percent in 2026 and to 6.3 percent in 2046; they would exceed tax revenues by 33 percent in 2026 and by 42 percent in 2046.

According to CBO’s projections, without changes in the programs, the balance of the DI trust fund will be exhausted in fiscal year 2022, the balance of the OASI trust fund will be exhausted in calendar year 2030, and the combined balances of the OASDI trust funds will be exhausted in calendar year 2029. If a trust fund’s balance declined to zero and current revenues were insufficient to cover benefits specified in law, the Social Security Administration would no longer be permitted to pay full benefits when they were due. In the years after a trust fund was exhausted, annual outlays would be limited to annual revenues: All receipts to the trust fund would be used, and the trust fund’s balance would remain essentially at zero. [Emphasis added.]

Thursday, December 22, 2016

CBO Projects A 29 Percent Cut In Social Security Benefits In 2030 When Trust Funds Are Depleted

From Congressional Budget Office, "CBO’s 2016 Long-Term Projections for Social Security: Additional Information" December 21, 2016 Report:

Sunday, December 18, 2016

Average And Total US Charitable Contributions Charts

From The Wall Street Journal, "The Mistakes We Make When Giving to Charity: Our minds play tricks on us, limiting the effectiveness of our efforts. But we can learn to do better." by Shlomo Benartzi and Christopher Olivola:

***

|

| Source: The Wall Street Journal |

|

| Source: The Wall Street Journal |

Saturday, December 17, 2016

Medium And Large US Airport Consumer Satisfaction Ranking: JD Power

From J.D. Power, Press Releases, "Airports Rise to Challenge of Higher Traveler Volume, Aging Infrastructure:"

***

Portland International Ranks Highest in Satisfaction among Large Airports; Indianapolis International Ranks Highest among Medium Airports

COSTA MESA, Calif.: 15 Dec. 2016 — Even with an increased number of travelers moving through airports—many of which are not designed for the volume of people and flights they now support—satisfaction with their airport experience is improving, according to the J.D. Power 2016 North America Airport Satisfaction Study,SM released today.

Overall traveler satisfaction with the airport experience averages 731 (on a 1,000-point scale) in 2016, an improvement from 725 in 2015. Overall satisfaction with large airports1 is 724, a 5-point increase from 2015, and satisfaction with medium airports is 760, an 8-point rise. The increase in satisfaction comes at a time when airports are posting a 5-6% annual increase in traveler volumes.

“Many airports, especially the nation’s largest airports, were never built to handle the current volume of traveler traffic, often exceeding their design limits by many millions of travelers,” said Michael Taylor, director of the airport practice at J.D. Power.

|

| Source: J.D. Power |

|

| Source: J.D. Power |

Thursday, December 15, 2016

US Net Emissions Of CO2 Equivalents Downward Trending And Declining Since Year 2000

From The Wall Street Journal, Real Time Economics, "White House Economists Spell Out the Four Most Stubborn Economic Challenges: Economists pinpoint productivity, income inequality, workforce participation and sustainability as areas of focus" by Nick Timiraos:

The White House released Thursday its annual Economic Report of the President, the last such volume produced by the Obama administration. While the nearly 600-page report catalogs what the administration views as its greatest successes, it also neatly frames what White House economists see as the most stubborn challenges facing economic policy.

***

Source: The Wall Street Journal

Average Household Debt Chart

From Bloomberg, "Do You Have More Debt Than the Average American? Here come the interest rate increases. Good time to size up your borrowings." by Suzanne Woolley:

The household debt numbers, in a new Nerdwallet report, come as paying off debt is set to become more costly.

***

Source: Bloomberg

Saturday, December 10, 2016

Bob Dylan's Nobel Prize In Literature Banquet Speech, December 10, 2016

From The Nobel Prize Organization, "Bob Dylan - Banquet Speech". Nobelprize.org. Nobel Media AB 2014. Web. 10 Dec 2016:

Bob Dylan - Banquet Speech

© The Nobel Foundation 2016.Banquet speech by Bob Dylan given by the United States Ambassador to Sweden Azita Raji, at the Nobel Banquet, 10 December 2016.

General permission is granted for immediate publication in editorial contexts, in print or online, in any language within two weeks of December 10, 2016. Thereafter, any publication requires the consent of the Nobel Foundation. On all publications in full or in major parts the above copyright notice must be applied.

Good evening, everyone. I extend my warmest greetings to the members of the Swedish Academy and to all of the other distinguished guests in attendance tonight.

I'm sorry I can't be with you in person, but please know that I am most definitely with you in spirit and honored to be receiving such a prestigious prize. Being awarded the Nobel Prize for Literature is something I never could have imagined or seen coming. From an early age, I've been familiar with and reading and absorbing the works of those who were deemed worthy of such a distinction: Kipling, Shaw, Thomas Mann, Pearl Buck, Albert Camus, Hemingway. These giants of literature whose works are taught in the schoolroom, housed in libraries around the world and spoken of in reverent tones have always made a deep impression. That I now join the names on such a list is truly beyond words.

I don't know if these men and women ever thought of the Nobel honor for themselves, but I suppose that anyone writing a book, or a poem, or a play anywhere in the world might harbor that secret dream deep down inside. It's probably buried so deep that they don't even know it's there.

If someone had ever told me that I had the slightest chance of winning the Nobel Prize, I would have to think that I'd have about the same odds as standing on the moon. In fact, during the year I was born and for a few years after, there wasn't anyone in the world who was considered good enough to win this Nobel Prize. So, I recognize that I am in very rare company, to say the least.

I was out on the road when I received this surprising news, and it took me more than a few minutes to properly process it. I began to think about William Shakespeare, the great literary figure. I would reckon he thought of himself as a dramatist. The thought that he was writing literature couldn't have entered his head. His words were written for the stage. Meant to be spoken not read. When he was writing Hamlet, I'm sure he was thinking about a lot of different things: "Who're the right actors for these roles?" "How should this be staged?" "Do I really want to set this in Denmark?" His creative vision and ambitions were no doubt at the forefront of his mind, but there were also more mundane matters to consider and deal with. "Is the financing in place?" "Are there enough good seats for my patrons?" "Where am I going to get a human skull?" I would bet that the farthest thing from Shakespeare's mind was the question "Is this literature?"

When I started writing songs as a teenager, and even as I started to achieve some renown for my abilities, my aspirations for these songs only went so far. I thought they could be heard in coffee houses or bars, maybe later in places like Carnegie Hall, the London Palladium. If I was really dreaming big, maybe I could imagine getting to make a record and then hearing my songs on the radio. That was really the big prize in my mind. Making records and hearing your songs on the radio meant that you were reaching a big audience and that you might get to keep doing what you had set out to do.

Well, I've been doing what I set out to do for a long time, now. I've made dozens of records and played thousands of concerts all around the world. But it's my songs that are at the vital center of almost everything I do. They seemed to have found a place in the lives of many people throughout many different cultures and I'm grateful for that.

But there's one thing I must say. As a performer I've played for 50,000 people and I've played for 50 people and I can tell you that it is harder to play for 50 people. 50,000 people have a singular persona, not so with 50. Each person has an individual, separate identity, a world unto themselves. They can perceive things more clearly. Your honesty and how it relates to the depth of your talent is tried. The fact that the Nobel committee is so small is not lost on me.

But, like Shakespeare, I too am often occupied with the pursuit of my creative endeavors and dealing with all aspects of life's mundane matters. "Who are the best musicians for these songs?" "Am I recording in the right studio?" "Is this song in the right key?" Some things never change, even in 400 years.

Not once have I ever had the time to ask myself, "Are my songs literature?"

So, I do thank the Swedish Academy, both for taking the time to consider that very question, and, ultimately, for providing such a wonderful answer.

My best wishes to you all,

Bob Dylan

Tuesday, December 6, 2016

Affordable Health Care, Not Affordable Health Insurance, Is The Problem

In reforming our expensive health care system, politicians and health care experts overly emphasize health insurance. Our fundamental problem is health care costs and not health insurance costs.

Health Insurance Is Reimbursement

Health insurance is a way to reimburse us for our health care costs. Total health insurance premiums plus out of pocket medical costs for the US population can never be less than the total health related costs for the same population. If it were, some medical service providers would go unpaid.

Competition in the health insurance arena does not increase competition among health care providers and will not lower the costs of providing health care.

Our politicians can hide some of the premiums of health insurance by using tax dollars and deficit financing borrowed funds for part of the premiums, but the total health care cost we pay is not lowered. Expecting changes in the laws regulating health insurers to lower health care costs are equivalent to expecting changes in automobile insurance to lower the price of a new car.

US Health Expenditures In 2015

The data from The Center For Medicare & Medicaid Services below shows that, on average, an individual's health insurance premium should be around $10,000, or about $40,000 per year for a family of four.

From The Center For Medicare & Medicaid Services, Research, Statistics, Data and Systems, National Health Expenditure Data, Historical, Highlights:

Increasing competition among health care insurers or other changes in the laws governing these insurers will not lower the amount the US spends on health care.

The US needs to lower the barriers to entry of health care providers to increase their numbers. The US also needs to remove barriers to competition among health care providers so as to lower the unit costs of health care and to increase the efficiency and the productivity of health care providers. We also need to enable individuals with less than a full medical degree to provide some of our routine medical diagnosis and care.

Increases in the number of health care providers and increases in their productivity are the only ways that the US will be able lower health related costs and make health care affordable for the average American.

Unfortunately, the Affordable Care Act failed to follow sound economic principles for lowering medical costs. Hopefully, future changes to our health laws will increase the number of health providers, make it easier to become a health provider, and foster greater competition among providers. With more providers and more competition among them, our health care and our health insurance will become affordable.

Health Insurance Is Reimbursement

Health insurance is a way to reimburse us for our health care costs. Total health insurance premiums plus out of pocket medical costs for the US population can never be less than the total health related costs for the same population. If it were, some medical service providers would go unpaid.

Competition in the health insurance arena does not increase competition among health care providers and will not lower the costs of providing health care.

Our politicians can hide some of the premiums of health insurance by using tax dollars and deficit financing borrowed funds for part of the premiums, but the total health care cost we pay is not lowered. Expecting changes in the laws regulating health insurers to lower health care costs are equivalent to expecting changes in automobile insurance to lower the price of a new car.

US Health Expenditures In 2015

The data from The Center For Medicare & Medicaid Services below shows that, on average, an individual's health insurance premium should be around $10,000, or about $40,000 per year for a family of four.

From The Center For Medicare & Medicaid Services, Research, Statistics, Data and Systems, National Health Expenditure Data, Historical, Highlights:

National Health Expenditures 2015 HighlightsIncreasing Competition

In 2015, U.S. health care spending increased 5.8 percent to reach $3.2 trillion, or $9,990 per person.

Increasing competition among health care insurers or other changes in the laws governing these insurers will not lower the amount the US spends on health care.

The US needs to lower the barriers to entry of health care providers to increase their numbers. The US also needs to remove barriers to competition among health care providers so as to lower the unit costs of health care and to increase the efficiency and the productivity of health care providers. We also need to enable individuals with less than a full medical degree to provide some of our routine medical diagnosis and care.

Increases in the number of health care providers and increases in their productivity are the only ways that the US will be able lower health related costs and make health care affordable for the average American.

Unfortunately, the Affordable Care Act failed to follow sound economic principles for lowering medical costs. Hopefully, future changes to our health laws will increase the number of health providers, make it easier to become a health provider, and foster greater competition among providers. With more providers and more competition among them, our health care and our health insurance will become affordable.

Wednesday, November 30, 2016

Wisconsin Has Largest Union Membership Decline In US After Walker's 2011 Reforms

From The Wall Street Journal, Opinion, "Wisconsin’s Reform Lesson: Scott Walker’s union reform has yielded huge political benefits:"

[Wisconsin Governor Scott] Walker’s 2011 reforms, known as Act 10, removed the ability of public unions to collectively bargain for benefits and required that unions be recertified every year by a majority of all members. The law ended the government’s role as the union’s automatic dues collector, and in 2015 Wisconsin also became a right-to-work state.

Given a choice for the first time, workers have left the union in droves. A recent analysis by the Milwaukee Journal Sentinel found that since 2011 the state has seen the largest decline in the country in the concentration of union members in the workforce. By 2015 union members made up some 8.3% of workers in Wisconsin, down from 14.2% before Mr. Walker’s reforms. The Badger State has some 187,000 fewer union members than in 2005, and the Milwaukee Teachers’ Education Association has lost some 30% of its members.

Unions still have clout but they must now operate on the same footing as other groups that represent member interests—such as trade associations—by providing services in exchange for financial support. [Emphasis added.]

The Problem With Charitable Tax Deductions

A comment I posted on Arnold Kling's askblog on December 1, 2012, "The Tax Deduction for Charitable Contributions:"

A problem with charitable deductions is that it is focused on organizational structure and not actions. If I invite and feed a poor person in my house on Thanksgiving, the tax deduction is not available. If I donate food or money to a food bank or church that feeds the same person on Thanksgiving, I get a deduction.A reader of askblog posted a reply that enhanced my comment:

I get a deduction for giving money to the Red Cross, but do not get a deduction for donating blood to the Red Cross.

If I grocery shop or cook a meal for a needy, ill senior in my neighborhood, no deduction, If I donate to a community organization that has volunteers who do the same thing, I get a deduction.

Charitable deductions are a disincentive to community and social responsibility.

When there is suffering, such as the Haiti earthquake, do we need a tax deduction to motivate us to send money, food, and other items? Of course not.

Let’s eliminate the charitable deduction. If the government takes too much money from us so that we cannot donate as much as we would like to charities, let’s fight for lower taxes and not more deductions.

Rick Weber on December 3, 2012 at 6:49 am said:

Your point about structure is spot on! A deduction (or credit) is a subsidy (so we get more charity, which is nice) but access to that subsidy requires organizations to meet the unavoidably bureaucratic rules of the subsidizer. The outcome may result in less effective output than if there were no subsidy at all, in addition to any number of adverse unintended consequences such as an increase in the relative cost of directly touching someone’s life.

Saturday, November 26, 2016

2016 Presidential Voter Breakdown By Socioeconomic Group And Percent Change

From The Wall Street Journal, "Vote Breakdowns Show How Parties Changed With Trump, Clinton at Top of Ticket: Democratic Party relied more on women and Americans with advanced college degrees, while the GOP depended on men and voters with some college experience" by Aaron Zitner:

The picture of the two parties comes from exit polls conducted during the past two elections. Those polls show whether Mr. Trump or Mrs. Clinton won a particular voter group.

*** In addition, the polls show the makeup of each political party—what share of its members come from which voter groups.

Source: The Wall Street Journal

Friday, November 25, 2016

My Unconventional Comment To Peggy Noonan's Opinion Piece On Trump's Conflict of Interests In The Wall Street Journal

My unconventional comment to The Wall Street Journal, Opinion, "No More Business as Usual, Mr. Trump: He has to abandon his company in order to deal on the country’s behalf." by Peggy Noonan:

If Trump does well as the President of the US, every item, hotel and rental property with or associated with the Trump name will increase in status and also will be more valuable. If he does poorly as the US President, every Trump item and property will be less valuable. He is probably the only US president who has ever had the equivalent of an equity stake in the success of his presidency, the future of the US economy and the global success of US foreign policy. He is probably the only US president who while in office has monetary incentives to do the right thing for the US. Unless Trump is promising to a foreign country some specific US governmental benefit, such as foreign aid, US military support, easier immigration to the US, ignoring human rights violations, etc., in return for a Trump Inc benefit, there is no conflict in continuing his Trump holdings. Unless Trump is following or recommending policies that solely benefit Trump holdings there are no conflict of interests.

Wednesday, November 23, 2016

Who In The US Has Not Read A Book In The Past 12 Months?

From Pew Research Center, "Who doesn’t read books in America?" by Andrew Perrin:

About a quarter of American adults (26%) say they haven’t read a book in whole or in part in the past year, whether in print, electronic or audio form. So who, exactly, are these non-book readers?

Source: Pew Research Center

Friday, November 18, 2016

Sources Of US Energy And Life-Cycle Green-House Gas Emissions Chart

From The Wall Street Journal, Journal Reports: Energy, "Is Nuclear Power Vital to Hitting CO2 Emissions Targets? Supporters say nuclear plants are the best way to transition to a low-carbon future. Others argue the plants are too risky to keep in operation:"

|

| Source: The Wall Street Journal |

Thursday, November 10, 2016

Job Growth From New Firms At Lowest Level In Over 20 Years

From The Wall Street Journal, Real Time Economics, "Job Gains at Startups Are Way Down and That’s a Bad Sign: Job gains from new firms are at the lowest share of employment since 1992" by Anna Louie Sussman:

Job gains from new firms are at the lowest share of employment in over 20 years, another sign of the declining role entrepreneurship plays in the U.S. economy.

Job gains from opening establishments as a percentage of overall private-sector employment dropped to 1% in the first quarter of 2016, the lowest level recorded since the Labor Department began the data series in 1992, and half what it was at its peak.

Throughout the 1990s, the share hovered between 1.6% and 2%, and edged lower throughout the subsequent decade. Since 2009, when the economic recovery began, it held between 1.1% and 1.3%.***

Source: The Wall Street Journal

Monday, November 7, 2016

Trump Has 20 To 30 Percent Chance Of Winning The Presidency According To Online Betting Markets

As of 5 PM EST, November 7, 2016, Donald Trump has between a 20 and 30 percent chance of winning the US Presidential election, according to several online political betting sites.

The University Of Iowa's online political betting market, Iowa Electronic Markets, gives Donald Trump a 22.6 percent chance of winning the US presidential election.

The online Ireland company political betting site, Predictious, shows Trump's chances of winning between 27.4 percent and 29.9 percent (bid ask prices).

The online betting site, PaddyPower, has Trump's odds as winning as 10 to 3, which is equivalent to 23.1 percent chance of winning.

The University Of Iowa's online political betting market, Iowa Electronic Markets, gives Donald Trump a 22.6 percent chance of winning the US presidential election.

The online Ireland company political betting site, Predictious, shows Trump's chances of winning between 27.4 percent and 29.9 percent (bid ask prices).

The online betting site, PaddyPower, has Trump's odds as winning as 10 to 3, which is equivalent to 23.1 percent chance of winning.

Wednesday, November 2, 2016

Worldwide Mobile Web Browsing Has Surpassed Desktop Browsing: US Desktop Web Browsing Still Leads Over Mobile

From alphr, "Mobile browsing just overtook the desktop for the first time: The decline of the desktop just passed a major milestone" by Alan Martin:

October 2016 was the month smartphones and tablet web browsing finally took the [worldwide] lead [over desktops]: 51.3% to 48.7%.

***

|

| Source: alphr |

Monday, October 31, 2016

Highest Rent Metropolitan Areas For Low And Average Quality Apartments: Units That Are Old And Needing Renovation: Chart

From Bloomberg, "Two New Charts Prove San Francisco Rents Are Out of Control: It's getting even more expensive to live in the Bay Area." by Patrick Clark:

CoStar Group, a real estate data firm, uses a five-star system to rate multifamily properties based on architectural attributes, structural systems, amenities, and other traits. For instance, one star buildings require significant renovation or are functionally obsolete. Two star buildings are associated with phrases like “functional,” average,” and “aging.” Together, one- and two-star buildings account for roughly one-third of market rate multi-family units in the U.S. There are plenty of big cities, like Dallas, or Atlanta, where the average asking rents for such apartments are less than $800 a month.

In San Francisco, typical monthly rent for the metropolitan area’s most humble housing stock is more than three times that amount—a staggering $2,586.

Source: Bloomberg

Thursday, October 27, 2016

Social Security Funding Problem In 3 Pictures From BloombergPolitics

From BloombergPolitics, "How the Next President Could Save Social Security" by Dave Merrill and Chloe Whiteaker:

The problem

Since 2010, Social Security’s funding mechanism has been taking on water. The number of workers supporting a growing number of retiring baby boomers is not sufficient to pay all the benefits they are due.

Source: BloombergPolitics

‘Trust fund’ draw down

Since there are not enough payroll taxes being collected day-to-day, money is drawn from Social Security’s “trust fund” reserve to meet the shortfall. The $2.8 trillion reserve grew out of payroll tax increases initiated in 1984.

Source: BloombergPolitics

Reserve depletion, 2034

When the trust fund reserves are depleted in 2034, retirees will collect only what the workers’ payroll taxes can provide: about 79 percent of benefits. So, for example, instead of an annual $18,000 benefit, a retiree would receive $14,220.

Source: BloombergPolitics

Wednesday, October 26, 2016

74 Percent Of Voters Want Congressional Term Limits

From Rasmussen Reports, "More Voters Than Ever Want Term Limits for Congress:"

Voters agree more strongly than ever with the need for term limits but also still doubt Congress will go along with them.

A new Rasmussen Reports national telephone survey finds that 74% of Likely U.S. Voters favor establishing term limits for all members of Congress. Just 13% are opposed, while just as many (13%) are undecided.

Sunday, October 23, 2016

Iran, Not Russia, Hacked Democratic National Committee (DNC), Says John McAfee

From CYBERSECURITY BUSINESS REPORT, "John McAfee: 'Iran hacked the DNC, and North Korea hacked DYN' " by Steve Morgan:

John McAfee -- in an email exchange and follow up phone call just moments ago -- said sources within the Dark Web suggest it was Iran, and he absolutely agrees. While Russian hackers get more media attention nowadays, Iranian hackers have had their share.*** Earlier this year, Iranian hackers were charged by the U.S. Department of Justice (DOJ) over cyber attacks.*** What about Russia?

"If all evidence points to the Russians, then, with 100% certainty, it is not the Russians," said McAfee. "Anyone who is capable of carrying out a hack of such sophistication is also capable, with far less effort than that involved in the hack, of hiding their tracks or making it appear that the hack came from some other quarter. The forensic tools used to assign culpability in a hack are well known, in the cybersecurity world, to be largely ineffective. They may, sometimes, correctly identify an unsophisticated 15 year old as the source of a hack, such as the teenager who hacked the FBI less than a year ago. But they are completely ineffective against large, sophisticated groups of hackers such as those run by the Russian State."

Friday, October 21, 2016

Bank Fines Causing Slow Global Growth: Fines Reduced Global Lending Capacity To Real Economy By Over $5 Trillion

From The Wall Street Journal, "Bank Legal Costs Cited as Drag on Economic Growth: Fines on banks translate into $5 trillion of ‘reduced lending capacity,’ bank says" by Katy Burne and Aruna Viswanatha:

A heightened emphasis by banking regulators and law-enforcement officials on financial misconduct may be constraining global growth, some officials warn.

Legal expenses are among the burdens weighing on banks, policy makers say. “The roughly $275 billion in legal costs for global banks since 2008 translates into more than $5 trillion of reduced lending capacity to the real economy,” Minouche Shafik, a deputy governor of the Bank of England, told a New York conference of regulators and bankers Thursday.

Other policy makers have expressed concern that strict crackdowns on banks’ lapses in carrying out anti-money-laundering regulations have led banks to nearly cut off several emerging markets from the global financial system, damping their economies. The International Monetary Fund, in particular, has sounded that alarm repeatedly this year and held a conference highlighting the issue at its annual meeting in early October.

Thursday, October 13, 2016

Hillary's Tax Plan Will Lower GDP, Capital Investment, Jobs, Wages: Hillary's Tax Plan Will Lower Payroll Tax Revenue That Funds Social Security And Medicare

From Tax Foundation, "Details and Analysis of Hillary Clinton’s Tax Proposals, October 2016" by Kyle Pomerleau:

Economic ImpactPayroll taxes are used to fund Social Security and Medicare. Hillary's tax plan, through lower wages and fewer full-time equivalent jobs, will lower tax revenues to fund these two programs. Her plan will exacerbate the funding problem that Medicare and Social Security already have.

According to the Tax Foundation’s Taxes and Growth Model, Secretary Clinton’s tax plan would reduce the economy’s size by 2.6 percent in the long run (Table 2). The slightly smaller economy would lead to 2.1 percent lower wages, a 6.9 percent smaller capital stock, and 697,000 fewer full-time equivalent jobs. The smaller economy results from somewhat higher marginal tax rates on capital and labor income.

These projections are what we estimate would happen at the end of a ten-year period and are compared to the underlying baseline of what would occur absent any policy change. For example, the U.S. real GDP will grow by 19.2% from 2016-2025, according to the Congressional Budget Office (CBO), if policy remains unchanged. We predict that the reduced incentives to work, save, and invest would reduce the end-of-period GDP by 2.6 percent below the level it would have been without the policy change.

Revenue Impact*** On a dynamic basis, the plan would increase federal revenues by $663 billion over the next decade. The slightly smaller economy would reduce wages, which would narrow both the individual income and payroll tax bases. As a result, the individual income tax proposals would raise less than half as much revenue as they do under the static analysis, while payroll tax revenues would decline.

Wednesday, October 12, 2016

Hillary's Higher Income Tax Rate On The Very Rich Will Not increase Tax Revenues

"High Tax Rates Don’t Raise Receipts" from The Heritage Foundation, Federal Budget in Pictures:

High Tax Rates Don’t Raise Receipts

|

| Source: Heritage Foundation |

Tuesday, October 4, 2016

US Supreme Court Has Upheld Right Of Any Taxpayer To Decrease Or Avoid Taxes Altogether: Trump Is Just Doing What The US Supreme Court Has Said Is Legal For The Past 80 Years

From Justia, US Supreme Court, Gregory v. Helvering, 293 US 465 (1935):

The legal right of a taxpayer to decrease the amount of what otherwise would be his taxes, or altogether avoid them, by means which the law permits, cannot be doubted. United States v. Isham, 17 Wall. 496, 84 U. S. 506; Superior Oil Co. v. Mississippi, 280 U. S. 390, 280 U. S. 395-396; Jones v. Helvering, 63 App.D.C. 204, 71 F.2d 214, 217.As the most quoted lower court federal judge, Judge Learned Hand stated in the same case at the lower level federal appellate court, Helvering v. Gregory, 69 F.2d 809, 810 (2d Cir. 1934), aff'd, 293 U.S. 465 (1935):

Any one may so arrange his affairs that his taxes shall be as low as possible; he is not bound to choose that pattern which will best pay the Treasury; there is not even a patriotic duty to increase one's taxes. U. S. v. Isham, 17 Wall. 496, 506, 21 L. Ed. 728; Bullen v. Wisconsin, 240 U.S. 625, 630, 36 S. Ct. 473, 60 L. Ed. 830. Therefore, if what was done here, was what was intended by section 112 (i) (1) (B), it is of no consequence that it was all an elaborate scheme to get rid of income taxes, as it certainly was.

Saturday, September 17, 2016

Illinois Pension Switches From Active Managed To Passive Index Funds: Fees Drop 90 Percent

From The Wall Street Journal, "Illinois State Pension Board Stops Trying to Beat the Market: Switch to funds that track market is a win for Vanguard Group, Northern Trust; among the losers: T. Rowe Price, Fidelity" by Timothy W Martin:

The board overseeing 401(k)-style benefits for 52,000 Illinois state workers has terminated all money managers who try to handpick winners, a major embrace of low-cost funds that instead mimic the markets.*** The shift would dramatically reduce outside management fees paid plan-wide, dropping from more than $10 million annually to $1 million, Marc Levine, the board’s chairman, said in an interview. On a per-participant basis, it equates to fees being shaved to about one-fourth of the previously paid total.*** The Illinois plan’s abandonment of higher-charging, so-called “active” managers comes amid a broader debate unfolding among big investors: whether Wall Street firms can consistently outperform a simple index fund that costs virtually nothing.

Tuesday, September 13, 2016

My Posted Comment To Megan McArdle's Bloomberg Article, "Banks and Colleges Are Wasting Our Money"

My posted comment to Megan McArdle's article, "Banks and Colleges Are Wasting Our Money" on BloombergView:

When there are rents and barriers to entry, innovators attempt, sometimes successfully and sometimes not, to develop less costly and/or higher quality substitute products. We get email, text message, Skype, YouTube, Uber, Kickstarter, Makerbot, Bitcoin, Netflix, streaming music services, etc. All are less costly and/or have better benefits than their prior alternatives.

In 1971, the US Supreme Court case of Griggs v Duke Power Co effectively banned employer aptitude testing of applicants. Employers had to resort to other signals about applicants and the college graduation race began. Colleges with their judicially created oligopoly became free to increase tuition without the possibility of employers developing their own alternative applicant aptitude signal. Students left with no other employer signaling mechanism are left with little choice but to pay the higher tuition.

Thursday, September 8, 2016

CBO's Projects Slower GDP Growth Due To Retiring Baby Boomers, Stable Participation Rate Of Working-Age Women, Work Disincentives Of Federal Taxes And Spending, Lower Productivity, And Crowding Out Of Private Investment By Federal Borrowings

From Congressional Budget Office, "Why Is CBO’s Projection of GDP Growth Slower Than Past Rates of Growth?" Posted by Robert Shackleton, analyst in CBO’s Macroeconomic Analysis Division, on September 8, 2016:

According to CBO’s most recently published projections, the economy is expected to grow substantially more slowly over the coming decade than it has over much of recent history. Whereas inflation-adjusted gross domestic product (GDP) grew by an average of 3.2 percent per year from 1950 to 2015—which is about the same as the average growth rate during the 25 years preceding the 2007–2009 recession—CBO expects that it will grow by only 2.0 percent per year over the coming decade.

In large part, the projected slowdown in economic growth is due to slower growth in the labor force. During the 1950–2015 period, growth was spurred by two factors: the large increase in the working-age population that was caused by the post–World War II baby boom and the rapid rise in women’s participation in the labor force. Driven by those factors, the labor force grew by an average of about 1½ percent per year from 1950 to 2015; the average rate of annual growth in the 25 years preceding the last recession was only slightly lower. More recently, the ongoing retirement of the baby boomers and the relatively stable labor force participation rate of working-age women have led to a decline in labor force growth. Because those trends are expected to continue, CBO projects that the labor force will grow at an average rate of only about ½ percent per year over the next decade. In addition to demographic factors, that projection reflects CBO’s judgment that some people will decide to work somewhat less because of federal tax and spending policies that are set in current law.

Slower growth in the labor force accounts for only about three-fifths of the projected slowdown in the growth of inflation-adjusted GDP; slower growth in labor force productivity accounts for the rest. Labor force productivity grew by an average of about 1¾ percent per year from 1950 to 2015; the average rate of annual growth was about the same in the 25 years preceding the last recession. However, CBO projects that labor force productivity will grow at an average annual rate of less than 1½ percent over the coming decade. That slowdown is attributable mainly to two other projections that CBO has made—namely, that growth in both capital services and total factor productivity (TFP, or output per unit of combined labor and capital services) in the nonfarm business sector of the economy will also be slower. Those projections reflect CBO’s expectation that some of the unusually slow growth of TFP during the past decade will persist over part of the next decade. They also reflect the agency’s projection of greater federal borrowing under the current laws governing taxes and spending, which would crowd out some private investment.

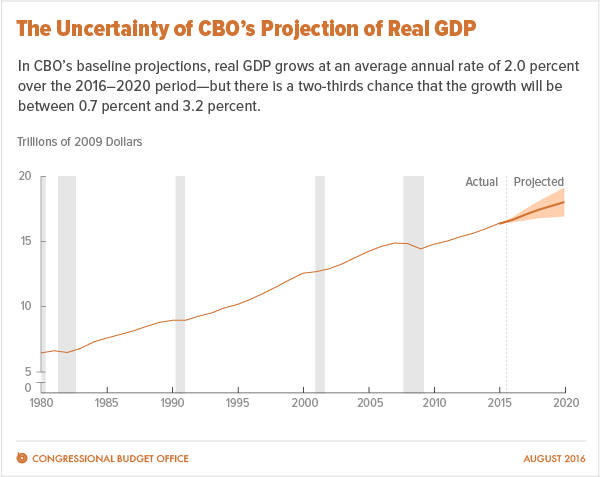

Uncertainty And Standard Deviations Of CBO's Forecasts Of Real GDP And Inflation

From Congressional Budget Office, "Uncertainties in the Economic Outlook" Posted by Charles Whalen, analyst in CBO’s Macroeconomic Analysis Division, on September 7, 2016:

On August 23, CBO published An Update to the Budget and Economic Outlook: 2016 to 2026, describing the agency’s projections for the federal budget and the U.S. economy over the next 10 years. As is always the case, economic outcomes will undoubtedly differ from CBO’s projections in some respects. Today, we discuss several uncertainties in the current economic outlook.*** Uncertainties

Recognizing the uncertainty of economic forecasts, CBO constructs its projections so that they fall in the middle of the distribution of possible outcomes, given current law and the economic data available when the projections are prepared. Nevertheless, many developments—such as economic growth abroad that was weaker than expected or growth in productivity that was faster than expected—could make outcomes differ substantially from what CBO has projected.*** To roughly quantify the degree of uncertainty in its projections for the next five years, CBO analyzed its past forecast errors for the growth rate of real GDP over five-year periods since 1976. Those errors have a standard deviation of about 1.3 percentage points: Thus, in CBO’s view, there is a two-thirds chance that the average annual growth rate of real GDP over the next five years will be between 0.7 percent and 3.2 percent (see the figure). Similarly, CBO’s forecast errors for inflation over five-year periods (as measured by the consumer price index for all urban consumers, which is generally higher than the PCE price index by about 0.4 percentage points per year owing to the different methods used to calculate them) have a standard deviation of 1.5 percentage points, which suggests that there is a two-thirds chance that inflation will average between 0.6 percent and 3.6 percent over the next five years.

Source: Congressional Budget Office

Thursday, September 1, 2016

Chart Of 2001 To 2014 Immigrant Deportations By US Department Of Homeland Security

From Pew Research Center, "U.S. immigrant deportations declined in 2014, but remain near record high" by Ana Gonzalez-Barrera and Jens Manuel Krogstad:

Source: Pew Research Center

The Obama administration deported 414,481 unauthorized immigrants in fiscal year 2014, a drop of about 20,000 (or 5%) from the prior year, newly released Department of Homeland Security data show. A total 2.4 million were deported under the administration from fiscal 2009 to 2014, including a record 435,000 in 2013, according to a Pew Research Center analysis of the data.

"What Is Productivity?" New Video From US Bureau Of Labor Statistics

Fro US Bureau of Labor Statistics a new video, "What Is Productivity?"

The BLS productivity program is proud to release the video, “What is Productivity?” This video is intended to provide basic productivity concepts to a general audience and explain how growth in productivity leads to improvements in our lives. You can view the video at https://youtu.be/rIG237BJXQot

Tuesday, August 30, 2016

Reprint Of My June 1996 Letter To The US Treasury On The Need For GDP Indexed US Bonds Included In My Comment On Issuing Inflation Indexed Treasury Bonds

The following is a reprint of a letter I sent to the US Treasury on June 5, 1996, in response to its request for comments and information on inflation indexed bonds. At the time, Treasury was considering publishing a proposal on the details of issuing US government inflation indexed bonds. Included about midway through my comment is my still relevant recommendation for the issuance of GDP indexed bonds and bonds indexed to other economic indicators.

If a market for traded US GDP indexed bonds existed today, there would be much more certainty about the trajectory of short-term and long-term future US economic growth

Milton Recht

XXXXXXXXXXXXXX

XXXXXXXXXXXXXX, NY xxxxx

June 5, 1996

The Government Securities Regulations Staff

Bureau of the Public Debt

999 E Street NW

Room 515

Washington, DC 20220

Dear Sir:

I am writing to comment on the Treasury Department’s proposal to issue a new type of United States Government bond that adjusts for the effects of inflation. My comments relate to the riskiness, structure, and uses of an inflation indexed treasury bond.

RISK

One of the purposes motivating the planned issuance of an inflation protected bond is the protection of investors, both individual and institutional, from the risk of an unanticipated loss of purchasing power due to unforeseen inflation over the life of a bond. Expected inflation, as you well know, is already included in the expected yield of the bond. Implicit in the Treasury Department’s attempt at purchasing power protection is the assumption that protection against inflation shocks reduces the riskiness of the investment security.

Volatility or the standard deviation of the total return of a bond is a yardstick for gauging the risk of a potential decline in market value and a capital loss, and while an inflation indexed treasury bond does not yet trade in this country, estimates can be made of its expected volatility. Using data from Ibbotson, Stock Bonds Bills and Inflation 1996 Yearbook, the standard deviation of the total return of a treasury bond from 1929 to 1995 is 9.2% per year. The standard deviation of the CPI for the same period is 4.6% per year. A real return can be derived by removing inflation from the nominal return, and the standard deviation of the real return series can be measured. Due to the negative correlation between inflation and the computed total real return on a treasury bond, the standard deviation of the computed real return, which is the equivalent of an inflation adjusted bond, is higher than a regular treasury bond and is 10.6%. The implication is that an inflation adjusted bond will be about 15% riskier due to increased volatility than a regular treasury bond. This will most likely be true even if historical CPI has been overstated and is restated. Since inflation has a dampening effect on the total nominal return, and since real returns are more volatile than nominal returns, an inflation bond does not protect against purchasing power loss when the increase risk of capital loss is also considered. Marketing the bond as purchasing power protection without mentioning the increased risk of prior to maturity principal loss is misleading to the average investor, and a misleading statement by a mutual fund. The point is particularly important to mutual fund investors since the funds are constantly rolling over maturing debt into new securities and are maintaining a relatively constant average maturity and duration. An inflation indexed bond also will increase the cost of hedging for those institutions that will hold inflation indexed bonds, and that manage their asset liability mix, such as banks, savings institutions, and insurance companies.

CHOICE OF INDEX

If minimizing risk is one of the goals of issuing an inflation bond, than the choice of an inflation index should be partially determine by an objective measure of risk. The selection of an index, whether CPI, PPI, or GDP Deflator, should be based in part on which one of the many indices minimizes the volatility of the total real return of the bond, while providing an accurate measure of inflation.

RATIONAL EXPECTATIONS

All publicly traded securities, particularly those that trade in highly liquid markets with the availability of short-selling, contain in their prices the market’s expectations of the future outcomes of the states of the economy over the life of the bond. This concept of expectations theory and efficient market theory has been well studied and documented and generally applies quite well to the treasury market. The market does not make these expectations readily observable other than by changes in the price of the bond or equity.

The issuance of an inflation pegged security by the government is an important milestone for allowing the observation of the market’s forecast of important economic variables, such as inflation expectations, that impact public policy and debate. By comparing a zero coupon treasury bond with the equivalent maturity zero coupon inflation indexed bond, the market’s expectation of average inflation over that period until maturity can be determined. (Estimations of any tax effects can also be made so that they can be removed to get a truer picture of expected inflation.) This expectation of inflation will represent a politically and statistically unbiased best guess of inflation which will incorporate all available information about the future of the economy, which will quickly respond positively or negatively to anticipated policy changes, and which could be an important tool for the setting of monetary policy. It would therefore be useful to have zero coupon inflation bonds of several different maturities outstanding at any time.

INFLATION OR ANOTHER ECONOMIC INDICATOR

When viewed with the perspective that the issuance of an inflation indexed bond is a method of risk reduction and information gathering for policy formation, the fundamental question is whether inflation is the most important economic variable for risk protection and information gathering, or whether another economic variable as an adjustment factor for a treasury bond would serve more useful purposes and be better for the nation. Such a bond could be issued alone or with an inflation bond.

One of the greater problems for the U.S. in recent times has been the inability to achieve sustainable, strong, yet non-inflationary, economic growth. Strong economic growth, as you know, reduces the deficit problem, creates employment, increases real wages, increases tax revenues, and improves consumer confidence and a sense of well-being. The government and the private sector have been stymied by a lack of theory and knowledge about the best courses of actions to take to facilitate and achieve sustainable and strong growth in the economy.

Furthermore, the greatest risk that a business faces is usually that of a downturn in the economy, i.e. recession. A bond that was linked to the general economy, such as a bond whose interest payments were a fixed percentage of concurrently reported GDP, would act a barometer of future recessions and expansions. Zero coupon nominal GDP bonds in conjunction with zero coupon inflation bonds of the same maturities would allow the production of a yield curve of the future yearly expected growth rates of the economy, similar to the yield to maturity curves that are now produced using treasury bond data. The existence of a market in GDP linked bonds would allow short selling and the development of options on the bonds. Either of which could be used by businesses and individuals as hedges to reduce the effects of economic downturns. The information about future growth rates and the changes in the growth rates as policy changes are anticipated could be used by policy makers, academics, and the Federal Reserve to better understand the forces in our economy and to develop strategies for a long-term non-inflationary period of economic growth.

When shocks do occur to the economy, such as the oil price shocks of the 1970’s, the inflationary effects are much greater than would be anticipated by the price increase in the raw material or labor input. In fact, studies have shown that wage increases do not correlate with or predict future inflation, and that economic predictors based on historical or current data, such as the leading economic indicator index, are poor predictors of changes in the growth rate of the economy. Inflation in many cases, as in the 1970’s, represents a resource allocation problem as the economy makes a fundamental structural shift in its productive capacity. Therefore the risk that concerns individuals and the government is more closely aligned to GDP than an inflation index. Bonds linked to GDP would allow hedging of this risk and provide data on the market’s expectation of future economic growth. Reliable data about future economic growth would allow for better production planning and resource allocation which in themselves would substantially mitigate changes in prices and inflationary concerns.

RECOMMENDATION

The Treasury should issue inflation indexed bonds, particularly zero coupons bonds of differing maturities, but it should also recognize that the bonds’ volatility and therefore their risk may be greater than regular treasury bonds. The issuance of inflation indexed bonds is an important milestone for the issuance of bonds that can provide valuable information about the future of the economy, and consideration should be given to bonds linked to other economic variables. Bonds with an index linked to GDP may provide greater risk protection to businesses and individuals than inflation indexed bonds. GDP indexed bonds can provide reliable information about the future growth rates of the economy, and the improved accuracy of the information will lead to better production planning, resource allocation, and monetary policy, which will reduce inflationary pressures in the economy.

Thank you for reading my comments on an inflation adjusted bond. If any clarification is necessary, please feel free to contact me.

Sincerely,

/signed/

Milton Recht

If a market for traded US GDP indexed bonds existed today, there would be much more certainty about the trajectory of short-term and long-term future US economic growth

XXXXXXXXXXXXXX

XXXXXXXXXXXXXX, NY xxxxx

June 5, 1996

The Government Securities Regulations Staff

Bureau of the Public Debt

999 E Street NW

Room 515

Washington, DC 20220

Dear Sir:

I am writing to comment on the Treasury Department’s proposal to issue a new type of United States Government bond that adjusts for the effects of inflation. My comments relate to the riskiness, structure, and uses of an inflation indexed treasury bond.

RISK

One of the purposes motivating the planned issuance of an inflation protected bond is the protection of investors, both individual and institutional, from the risk of an unanticipated loss of purchasing power due to unforeseen inflation over the life of a bond. Expected inflation, as you well know, is already included in the expected yield of the bond. Implicit in the Treasury Department’s attempt at purchasing power protection is the assumption that protection against inflation shocks reduces the riskiness of the investment security.

Volatility or the standard deviation of the total return of a bond is a yardstick for gauging the risk of a potential decline in market value and a capital loss, and while an inflation indexed treasury bond does not yet trade in this country, estimates can be made of its expected volatility. Using data from Ibbotson, Stock Bonds Bills and Inflation 1996 Yearbook, the standard deviation of the total return of a treasury bond from 1929 to 1995 is 9.2% per year. The standard deviation of the CPI for the same period is 4.6% per year. A real return can be derived by removing inflation from the nominal return, and the standard deviation of the real return series can be measured. Due to the negative correlation between inflation and the computed total real return on a treasury bond, the standard deviation of the computed real return, which is the equivalent of an inflation adjusted bond, is higher than a regular treasury bond and is 10.6%. The implication is that an inflation adjusted bond will be about 15% riskier due to increased volatility than a regular treasury bond. This will most likely be true even if historical CPI has been overstated and is restated. Since inflation has a dampening effect on the total nominal return, and since real returns are more volatile than nominal returns, an inflation bond does not protect against purchasing power loss when the increase risk of capital loss is also considered. Marketing the bond as purchasing power protection without mentioning the increased risk of prior to maturity principal loss is misleading to the average investor, and a misleading statement by a mutual fund. The point is particularly important to mutual fund investors since the funds are constantly rolling over maturing debt into new securities and are maintaining a relatively constant average maturity and duration. An inflation indexed bond also will increase the cost of hedging for those institutions that will hold inflation indexed bonds, and that manage their asset liability mix, such as banks, savings institutions, and insurance companies.

CHOICE OF INDEX

If minimizing risk is one of the goals of issuing an inflation bond, than the choice of an inflation index should be partially determine by an objective measure of risk. The selection of an index, whether CPI, PPI, or GDP Deflator, should be based in part on which one of the many indices minimizes the volatility of the total real return of the bond, while providing an accurate measure of inflation.

RATIONAL EXPECTATIONS

All publicly traded securities, particularly those that trade in highly liquid markets with the availability of short-selling, contain in their prices the market’s expectations of the future outcomes of the states of the economy over the life of the bond. This concept of expectations theory and efficient market theory has been well studied and documented and generally applies quite well to the treasury market. The market does not make these expectations readily observable other than by changes in the price of the bond or equity.

The issuance of an inflation pegged security by the government is an important milestone for allowing the observation of the market’s forecast of important economic variables, such as inflation expectations, that impact public policy and debate. By comparing a zero coupon treasury bond with the equivalent maturity zero coupon inflation indexed bond, the market’s expectation of average inflation over that period until maturity can be determined. (Estimations of any tax effects can also be made so that they can be removed to get a truer picture of expected inflation.) This expectation of inflation will represent a politically and statistically unbiased best guess of inflation which will incorporate all available information about the future of the economy, which will quickly respond positively or negatively to anticipated policy changes, and which could be an important tool for the setting of monetary policy. It would therefore be useful to have zero coupon inflation bonds of several different maturities outstanding at any time.

INFLATION OR ANOTHER ECONOMIC INDICATOR

When viewed with the perspective that the issuance of an inflation indexed bond is a method of risk reduction and information gathering for policy formation, the fundamental question is whether inflation is the most important economic variable for risk protection and information gathering, or whether another economic variable as an adjustment factor for a treasury bond would serve more useful purposes and be better for the nation. Such a bond could be issued alone or with an inflation bond.

One of the greater problems for the U.S. in recent times has been the inability to achieve sustainable, strong, yet non-inflationary, economic growth. Strong economic growth, as you know, reduces the deficit problem, creates employment, increases real wages, increases tax revenues, and improves consumer confidence and a sense of well-being. The government and the private sector have been stymied by a lack of theory and knowledge about the best courses of actions to take to facilitate and achieve sustainable and strong growth in the economy.

Furthermore, the greatest risk that a business faces is usually that of a downturn in the economy, i.e. recession. A bond that was linked to the general economy, such as a bond whose interest payments were a fixed percentage of concurrently reported GDP, would act a barometer of future recessions and expansions. Zero coupon nominal GDP bonds in conjunction with zero coupon inflation bonds of the same maturities would allow the production of a yield curve of the future yearly expected growth rates of the economy, similar to the yield to maturity curves that are now produced using treasury bond data. The existence of a market in GDP linked bonds would allow short selling and the development of options on the bonds. Either of which could be used by businesses and individuals as hedges to reduce the effects of economic downturns. The information about future growth rates and the changes in the growth rates as policy changes are anticipated could be used by policy makers, academics, and the Federal Reserve to better understand the forces in our economy and to develop strategies for a long-term non-inflationary period of economic growth.

When shocks do occur to the economy, such as the oil price shocks of the 1970’s, the inflationary effects are much greater than would be anticipated by the price increase in the raw material or labor input. In fact, studies have shown that wage increases do not correlate with or predict future inflation, and that economic predictors based on historical or current data, such as the leading economic indicator index, are poor predictors of changes in the growth rate of the economy. Inflation in many cases, as in the 1970’s, represents a resource allocation problem as the economy makes a fundamental structural shift in its productive capacity. Therefore the risk that concerns individuals and the government is more closely aligned to GDP than an inflation index. Bonds linked to GDP would allow hedging of this risk and provide data on the market’s expectation of future economic growth. Reliable data about future economic growth would allow for better production planning and resource allocation which in themselves would substantially mitigate changes in prices and inflationary concerns.

RECOMMENDATION

The Treasury should issue inflation indexed bonds, particularly zero coupons bonds of differing maturities, but it should also recognize that the bonds’ volatility and therefore their risk may be greater than regular treasury bonds. The issuance of inflation indexed bonds is an important milestone for the issuance of bonds that can provide valuable information about the future of the economy, and consideration should be given to bonds linked to other economic variables. Bonds with an index linked to GDP may provide greater risk protection to businesses and individuals than inflation indexed bonds. GDP indexed bonds can provide reliable information about the future growth rates of the economy, and the improved accuracy of the information will lead to better production planning, resource allocation, and monetary policy, which will reduce inflationary pressures in the economy.

Thank you for reading my comments on an inflation adjusted bond. If any clarification is necessary, please feel free to contact me.

Sincerely,

/signed/

Milton Recht

Monday, August 29, 2016

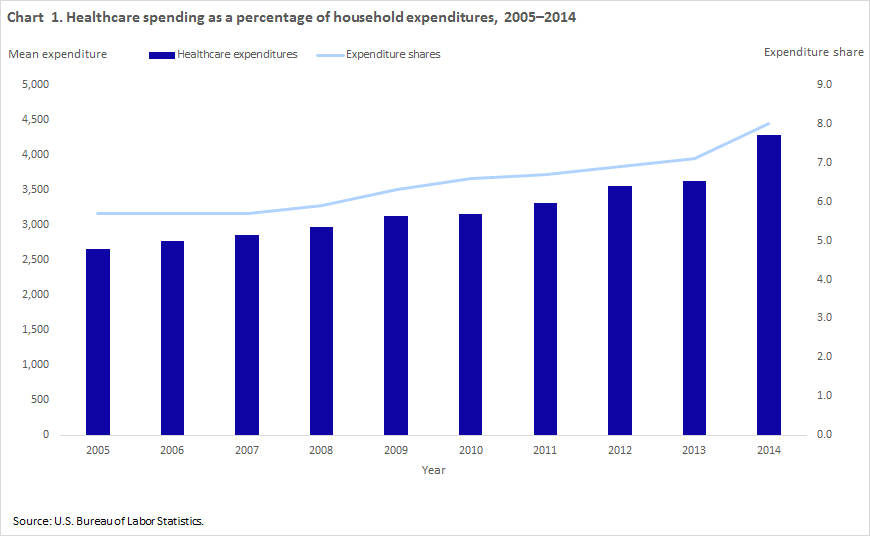

US Household Out Of Pocket Healthcare Spending Rose Steadily From 2004 To 2014 Despite Recession And Obamacare: Health Insurance Premiums Are Biggest Healthcare Expense For All Income Groups

From US Department of Labor, US Bureau of Labor Statistics, Beyond The Numbers, "Household healthcare spending in 2014" by Ann C. Foster:

Household healthcare spending has increased in dollar amount and as a share of household spending, even during the last recession when average household expenditures (and pretax income) declined. Consumer Expenditure Survey (CE) data show that household out-of-pocket healthcare spending rose steadily from an average of $2,664 (in nominal dollars) in 2005 to $4,290 in 2014 while the share of the household budget accounted for by healthcare spending held steady at 5.7 percent over the 2005–2007 period, but increased to 8 percent in 2014. (See chart 1.) In contrast, average total household expenditures rose from $46,409 in 2005 to $50,486 in 2008, then fell from 2009 to 2011. Spending increased to $51,442 in 2012, fell to $51,110 in 2013, and then rose once again to $53,495 in 2014.

Source: US Bureau of Labor Statistics *** Health insurance

Health insurance premiums accounted for the greatest proportion of healthcare spending among households at all income levels.This category includes spending for private health insurance obtained individually or through a group plan and for amounts for Medicare Part B and Part D coverage.

Subscribe to:

Posts (Atom)